The phrase danger in investments implies that any investment’s actual end result will differ from its anticipated end result, in different phrases it denotes the opportunity of loss incidence.

We usually associate investment danger with loss of capital, fluctuation or volatility in prices of listed securities, international change danger, inventory selecting danger and so forth. The effect of ‘illiquidity’ can be a necessary danger in listed securities like shares and exchange-traded funds (ETFs).

Real estate is plagued with illiquidity danger and that is nicely understood by most individuals, nonetheless, the identical parameter is considerably misunderstood in listed securities comparable to ETFs.

Generally in an hour of crisis, we could also be compelled to sell property like our home where because of illiquidity the ultimate realized sale worth could also be a lot lower than its fair value out there.

That is also referred to as misery promoting, whereby lack of liquidity out there (consumers) is chargeable for lower cost realization. The reverse will also be true whereby as a result of lack of liquidity a purchaser finally ends up paying a lot larger value as in comparison with the truthful worth of the asset.

So far as ETFs are involved one tends to give attention to the same old parameters comparable to the total expense ratio (TER) and tracking error (TE) of an ETF. However, ETF liquidity as measured by daily average volumes is probably one of the vital important components that an investor must contemplate when selecting the best ETF, i.e., inside its peer group.

The ‘trio’ of daily average volumes, TER and TE are ETF choice guidelines and analyzing these together inform us that, ‘all ETFs aren’t created equal.

Lack of liquidity as regards to listed securities like ETFs interprets right into an excessive ‘impact cost’ for each buyer and seller.

Impact cost represents the indirect cost of executing a transaction in a particular stock, or ETF, for a specific predefined order size, at any given point of time as in comparison with its ideal value. Impact cost is a sensible and lifelike measure of market liquidity.

For instance, the exchange terminal tells you that there’s the greatest buy order for 1,000 ETF units at ₹980 and greatest sell order for 2,000 ETF items at ₹982, therefore the perfect value outlined as the average of the most effective buy and sell order is ₹ 981 ( ₹980+ ₹982) / 2. However suppose you had been capable of buying 5,000 shares of ETF at a median value of ₹991, therefore your impact cost is 1% (991-981)/981. It means you incurred an indirect transaction cost of 1% to buy 5,000 shares due to the liquidity situations in that stock.

Nevertheless, if the identical security had excessive buying and selling volumes or excessive liquidity, then the execution price in case of buying or selling might have been comparatively decreased.

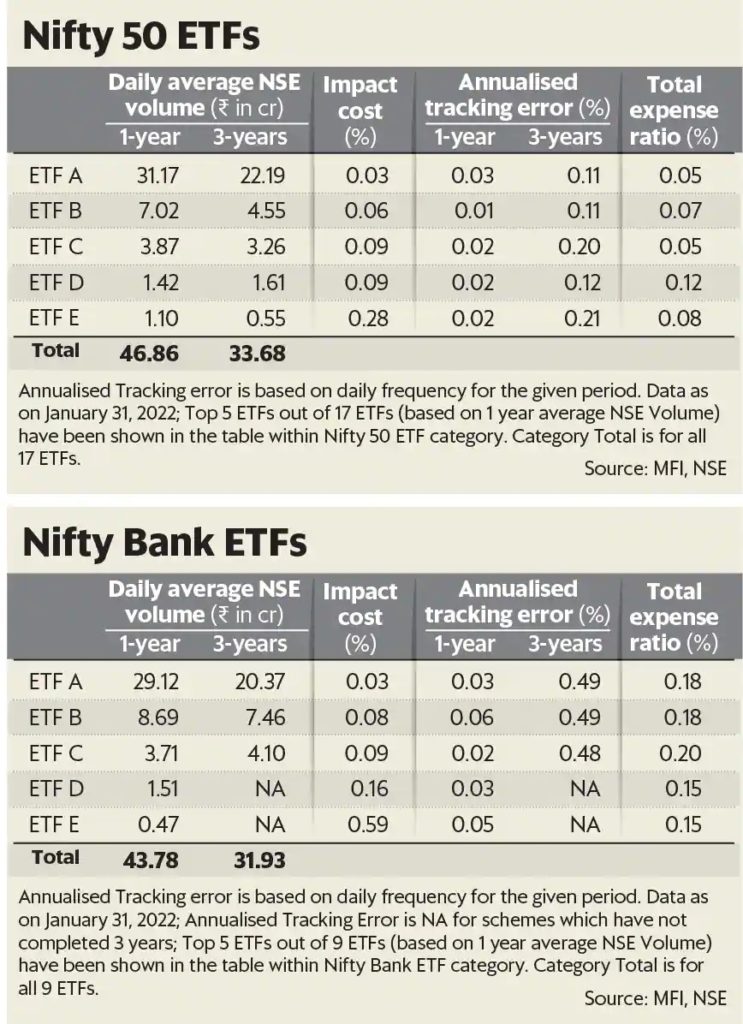

This bid-ask spread in case of an illiquid ETF is the fee that an investor has to bear for coming into or exiting the security in the secondary market. We are able to illustrate the above by taking the next examples of Nifty 50 and Nifty Bank ETFs. Nevertheless, as we dig deeper and observe the average daily volumes of every one of them, we discover a stark distinction. That is when the truth ‘all Nifty 50 ETFs are NOT created equal’ is clear.

ETF A has the highest daily average volume of 31.17 crores and 22.19 crores primarily based on twelve months and three years respectively, whereas ETF B has a volume of nearly 1/fifth of ETF A.

The above distinction will directly result within the comparatively decrease liquidity impact cost for ETF A, implying the lowest execution price for an investor as in comparison with its ideal price, relying on the quantum of order size.

That is akin to the distinction between liquid and illiquid shares – the former has decreased bid-ask spreads and due to this fact, entry/exit has a really low liquidity impact cost.

From this instance, we perceive that on account of high daily average volumes, Nifty 50 ETF A is the natural alternative for the investor.

We are able to take another instance to reaffirm this level and the next knowledge of Nifty Bank ETFs will make it clear.

‘All Nifty Bank ETFs are NOT created equal’ is illustrated by the highest daily average volumes of Nifty Bank ETF A as in comparison with its peers.

The selection of an ETF in its peer group is determined most significantly by daily average volumes.

An advantage because of lower TE and lower TER will get negated if the ETF doesn’t have enough liquidity, resulting in a high liquidity impact cost of the investor. One can conclude by saying that volumes are as important to an ETF as blood is to the physique.